The CAPE ratio, which looks at price-earnings multiples over a ten-year period (to smooth out the short-term ups and downs in the economy) is now above 37x. Since 1980, each time the multiple has been this elevated, investors suffered over the subsequent decade. This terrible track record is especially striking since the past 45 years have seen the largest increase in stock prices ever.

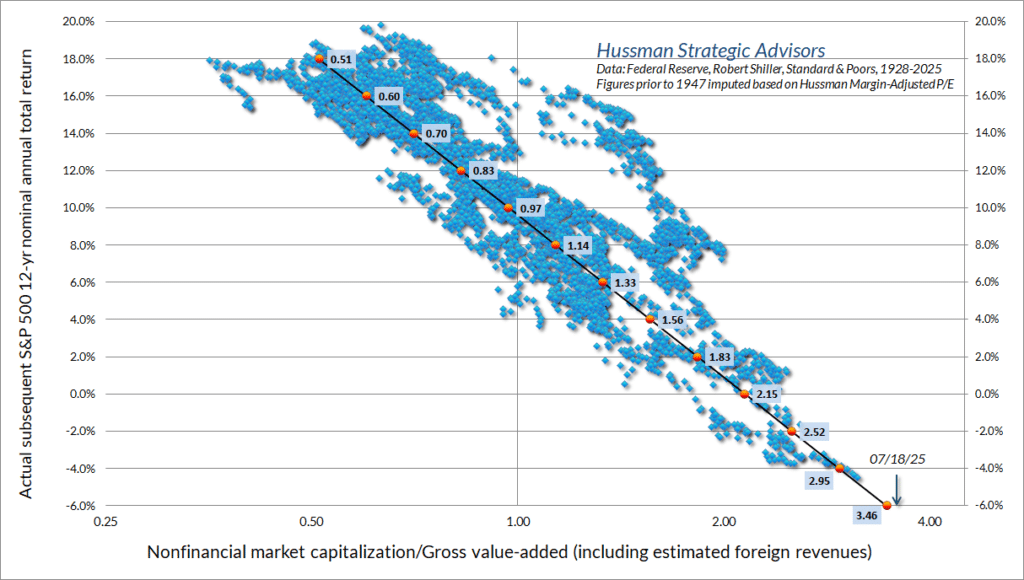

The highly regarded Buffett Indicator is even more cautionary. Though the chart below is overwhelming at first glance, its message is clear: looking at the results over many decades, the current level of the indicator – the arrow in the lower right – projects an average annual decline of 6% in the C Fund over the next dozen years.

“You can’t possibly call a bubble or a bust to the right day except once every several lifetimes,” said investing icon Jeremy Grantham in a recent interview. “What you can do, though, is to identify bubbles that eventually burst.”

The latest leg of our stock-market bubble – from mid-2020 to the present day – benefitted from good fortune, which in turn fueled enthusiasm to the point of euphoria. In late-March 2020, a massive (and rare) bipartisan bailout in conjunction with an unprecedented Fed easing lit the fuse under the stock market. By November, the rally was at risk: fair value had given way to overvaluation, and production was still at a standstill due to the pandemic. Fortunately, Covid vaccines were developed in record time – the first of which was announced on November 9th – restarting the world economy.

By the end of 2021, valuations hit extreme levels even as supply-shock inflation began its upward march. Central banks worldwide were slow to respond to the accelerating rise in prices – and when they did, fears grew that the spike in interest rates would trigger a global recession. The decline in stock prices in 2022 might have been the first leg of a multi-year bear market if not for the surprise announcement of ChatGPT. The seemingly unlimited potential of artificial intelligence reignited the market’s speculative instincts.

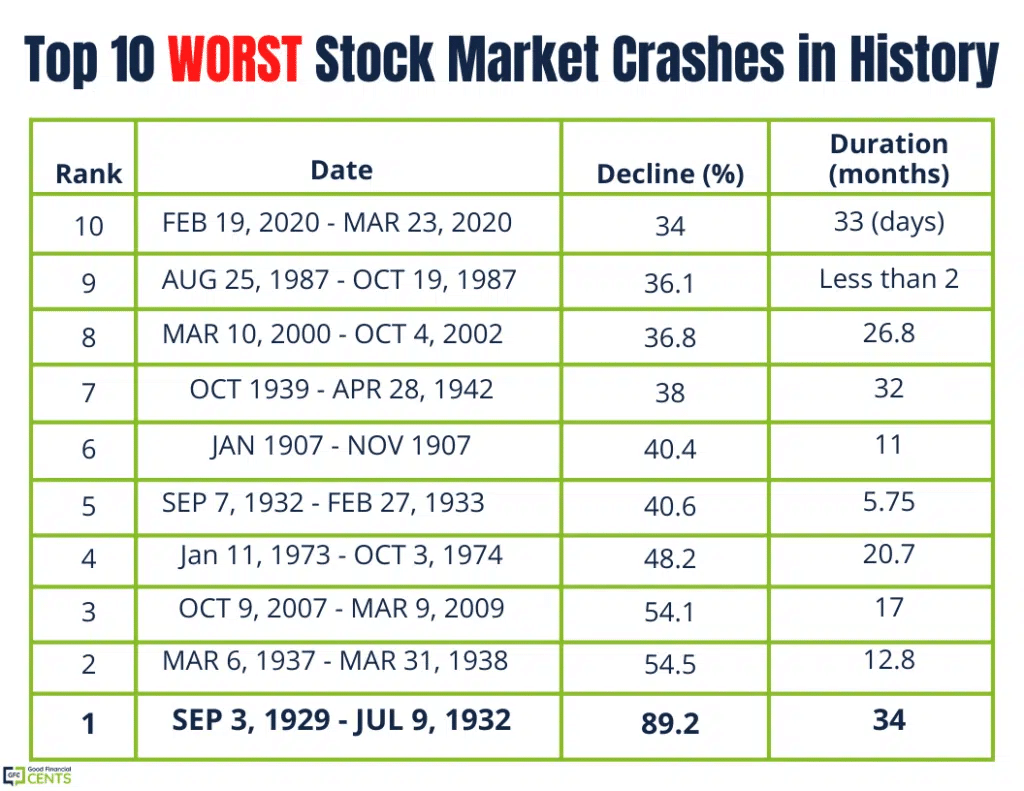

Although the major surprises these past five years have been favorable, history reminds us that the unexpected can turn against us as well. The Smoot-Hawley Act of 1930 transformed a business downturn into a global depression, taking the benchmark stock index almost 90% lower. The 1973 oil embargo ushered in a decade of severe stagflation and collapsed the stock & bond markets. In October 1987, the catastrophic failure of portfolio insurance was a key culprit in the worst single-day decline ever. Lehman Brothers’ bankruptcy in 2008 triggered both the Great Financial Crisis and the halving of the C Fund.

People generally believe that financial cycles are caused by hype that fails to materialize (such as dotcom fly-by-nights) but as Jeremy Grantham noted, most stock-market booms and busts are based on successful technologies: trans-Atlantic shipping in the 1700s, railroads in the 1800s, transportation & telecommunications in the 1900s, and the Internet this century.

Success breeds excess – competition causes creative destruction to profit margins and stock prices (“You didn’t need six railroads between Manchester and Leeds”). Notably, even the greatest success story of the past 30 years – Amazon – suffered a 92% price decline in the dotcom bust. Nonetheless, “we have such a desperate predisposition for good news,” says Grantham. “And no interest at all in the future – extrapolate today’s conditions forever. We never anticipate anything.

“The average investor is not worried until the hammer lands on the head, clearly and squarely,” he adds, warning that the rose-tinted bias applies even more forcefully to advisors. In his seven-decade tenure on Wall Street, Grantham has observed that investors freeze during bear markets, but during bull markets they actively seek up-trending stocks and upbeat advisors.

The danger here is two-fold: you can lose a lot of money in a bear market, and you can lose any desire to buy into the subsequent bull market. Most investors have little or no memory of the grim 2000-2003 sell-off, and the devastating effect on the collective psyche. The 2008-2009 bear market was essentially only six months (though it felt a lot longer), whereas the 2000 decline lasted a mere five weeks.

“Once in a blue moon, you get hit from every direction,” Grantham recalled, “not just on the head but here there and everywhere, and we exaggerate the bad news: 1974, been there done that, 7½ times very depressed earnings … 1982, 8 times very depressed earnings.” By contrast, “2000, 35 times very inflated earnings. We are not an organism trying to normalize, we double-count when given half a chance.”

“Serious measures of value say this is the highest-priced stock market in the history of the U.S. – this is not a good sign for long-term returns. It’s killing to get the timing right, but the consequences are never different. Always goes back to reasonable prices.”